The only thing worse than being blind is having sight but no vision – Helen Keller

With the chaos of balancing life with work or a business, spending time with family, kid activities, staying healthy, and fitting in personal interests it may seem impossible to focus on long-term dreams and goals. Just getting through each day or week can be a struggle.

However, if we don’t take the time to consider what we truly want in our lives, what will bring us the most happiness and joy, what we want to accomplish while on this earth, the liklihood of them happening is low. Some of those dreams could take a lifetime which requires us to have a long-term focus while taking the actions today to take us one step closer.

Regarding our financial success, it takes a similar approach to think long-term and implement strategies that positions us with the highest chance of success regardless of what happens. One concept that most people have likely heard of is the power of compound interest and the need to leverage it to build great wealth. However, there are many factors that can create headwinds to reaching your maximum financial potential and obtaining the true benefits of the compound interest curve.

It comes in two major forms…losses and use. In terms of losses, they can come in the form of taxes, fees, and market volatility which can greatly erode your wealth and slow the compounding. Exploring strategies to minimize these types of losses can leave more of your money working instead of being transferred to others.

The use of your money can reduce or reset the compound interest curve such that you’ll need more time to get the biggest benefits. It’s typically thought that it’s best to use your own money to finance a purchase or an investment, however the strategic use of other people’s money (OPM) can have a multiplier effect on your money. Look no farther than your local bank as they utilize this approach to earn substantial returns leveraging depositor funds instead of their own.

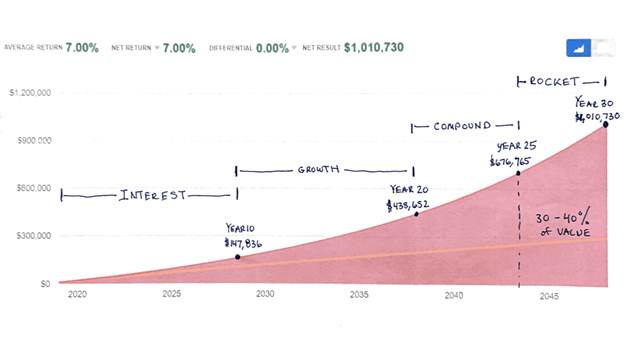

Now, understanding the phases of the compound interest curve can help you fully appreciate its power. In the below example, if you invested $10k per year for 30 years earning 7% you would reach over $1MM.

Phase 1 (Interest): In this phase your money starts to earn some interest and reaches a modest $148k with a total $100k contribution through the first 10 years. Not bad, but we’re just getting started.

Phase 2 (Growth): During the next 10 years, you’ll experience some growth in your wealth as your account reaches $439k. In this phase, the ratio of what you contribute and how much your account balance increases grows to nearly 1:3.

Phase 3 (Compound): In the next 5 years, we start to see the impact of the compounding of interest from the prior 20 years. At this phase, the account balance grows significantly to $677k (over a $238k gain with a $50k contribution). The consistent approach to saving and investing is really starting to take hold.

Phase 4 (Rocket): In this last 5 years is where nearly 30-40% of the value of the account will be realized and takes off. As noted before, getting here is the hard part as it not only takes time, but it also requires the avoidance of the losses and use of the money which will slow it down dramatically.

Now, when you take look at the compound interest curve, for each year this is delayed, what part of the curve do you not get to realize?

You guessed it, the end, and that’s where most of the value is created. You only have one compound interest curve in your lifetime; use it wisely and start as early as you can.