Although there are some positive developments such as increased vaccinations and hope for an improving economy, there is still so much uncertainty in our world today. However, in times like these, the key is to focus on the reality of the situation so we can pave a path toward progress and prosperity.

It’s really about control, and no philosophy addresses this better than Stoicism. The Stoics believe a variety of things, but most of them center around creating a strong internal locus of control.

An internal locus of control is when you have the belief that you are responsible for your success or failure in this world.

Life is putting forth a challenge summed up in one sentence: “Such and such happened. So what are you gonna do about it?”

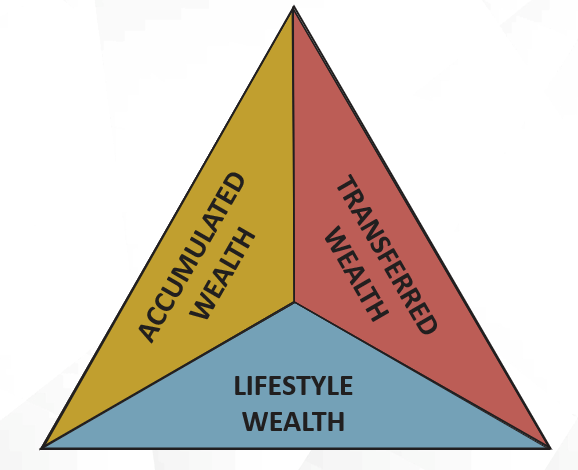

For those of your looking to take more control over your financial lives, understanding the three types of wealth is paramount. The below pyramid represents everything you’ve accumulated so far, and everything you will accumulate in the future.

For starters, Accumulated Wealth is what most typical financial advisors will target for their services. “Give me your money, and I’ll invest it for you,” is what you’ll likely hear. But there are other things that are even more important than what you’ve accumulated.

Lifestyle Wealth is a matter of making the distinction between needs and wants. Most financial professionals will tell you that you need to make sacrifices in your lifestyle wealth in order to achieve your goals. That may be true to some degree, however they may be overlooking something more important.

Transferred Wealth is money you don’t even know you’re losing or don’t recognize the true impact it can have to your wealth building. Getting a handle on this can have a massive impact to your ability to enjoy more today and save more for your future.

Even before the pandemic surfaced, many experts were warning investors to temper their expected returns for the decade ahead. Vanguard’s May 2020 Market Perspectives advised clients to reset their 10-year annualized returns on stocks to a range of 4.8% to 7.8% per year–and no more than 1.0% to 2.0% annually on U.S. bonds.

Many of you have been saving a decent amount of income for retirement—10% is not unusual. Congrats. But chances are you’re spending sizeable amounts of money on taxes and interest payments on your mortgages, home equity lines, college loans, car loans, credit cards and more. And that’s on top of your normal monthly living expenses.

While you want that 10% to grow, have you ever thought about all the little fees and expenses you pay that quietly eat away at your wealth? If you could efficiently chip away at all the hidden wealth eroders then you wouldn’t have to take on as much risk with your investments and constantly “chase returns” to make your nest egg grow.

Let’s take a closer look at some of the major hidden wealth eroders and see how you can attack them:

- Taxes Taxes are the biggest expense most of us face in our lifetimes. Imagine $1 doubling every year. Believe it or not, that $1 would be worth $1,024 dollars after 10 years. Sounds great, but with just a 10% tax rate on that money every year, your money would only be worth about $613 (40% less) after 10 years. After 20 years, the account would grow to over $1 million without tax, but would be worth only $376,000 (67% less) after factoring in a modest 10% tax rate. It’s even more sobering when you consider that taxes are likely to go up in light of $26 trillion in government debt, unfunded liabilities for social programs, historically low tax rates, etc.). Now is the time to explore ways to reduce your taxes by understanding what the government wants to incent (e.g. starting a business, owning rental real estate, giving to charities etc…).

- Fees on your investments. Even if you own “no load” mutual funds, it’s common to see “management fees” amounting to 1%-2% of your assets taken out of your account every year. Even a 1% management fee every year could be eroding over 20% of the value of your account over a 20- to 30-year period. Imagine the impact of a 2% or higher annual management fee?

This is a good time to take a hard look at the fees you’re paying on your various accounts. I know most investors don’t even know which fees they’re paying or how much their losing every year to the compound effect of those fees. But, even an extra 1% in fees every year can have a devasting effect on your wealth and retirement. Fees are a real opportunity cost. Ask yourself if you’re really getting added value for all those “management fees” and “transaction fees.” If not, there are plenty of other options that have extremely low fees or moderate fees that you really should explore with your advisor.

- Interest on auto loans, credit cards, student loans, HELOCs. I’ve come to understand that the way you use your money is more important than where you put it. Nothing demonstrates this more than financing all the things in your life. There are two primary ways we finance things:

1) We take on debt and pay back principal (with interest) or

2) We pay cash and avoid the interest payments.

As Nelson Nash, author of Becoming Your Own Banker writes, “you finance everything you buy…you either pay interest or pass it up.”

However, there’s a third way to finance things that can help you recapture significant interest cost. It allows your money to grow and compound continuously in a safe vehicle for long periods of time and use it as collateral to borrow from a financial institution. Having your money continuously earning will allow you to grab the magic of compound interest.

Opportunity cost

The reason I’m so adamant about focusing on all the hidden wealth eroders in our lives is that there’s a significant opportunity cost to ignoring those fees. Every dollar you pay out in unnecessary fees is a dollar you cannot use to make your money grow. Think about it like a $5 cup of coffee at Starbucks? Sure, it smells and tastes good when you first receive it from your friendly server in the morning. But what if you took that $5 and invested it instead in a simple index fund earning 5% a year? That $5 would be worth $21.61 in 30 years without lifting a finger. That’s an expensive cup of coffee at the Opportunity Cost Café. If you account for all the losses you may experience, the opportunity costs can result in massive wealth that gets transferred for the benefit of others.

Conclusion

When it comes to building wealth and achieving peace of mind, its’ not about how much money you make; it’s how do you make the most of your money. My video (Maximize Potential) has more. If you or someone close to suspects your money is not working as hard as it could be working for you, please don’t hesitate to call me.