Richard Kiyosaki, author of the best seller of “Rich Dad, Poor Dad” typically states that there are three sides to every coin (Heads, Tails, and The Edge). Your ability to understand contrasting points of view and your ability to glean what information you believe to be valuable from each side is a crucial skill.

This is key in all aspects of your life that you deem important and is especially important as it relates to your personal finances and wealth. Yes, it will require you take responsibility for your success, but the control, wisdom, and wealth can be so rewarding. Let’s get to work.

Key Takeaways

Unlike most other investments, real estate can generate multiple ways to build wealth along with tax benefits.

Real estate can be IDEAL for investors (Income, Depreciation, Equity, Appreciation and Leverage).

Over longer time periods, real estate has outperformed, bonds, Treasury bills, even stocks.

Stocks are likely to be very volatile for a while. Fixed income is yielding next to zero. If you’re frustrated by the lack of options for getting a decent return on your money (and still being able to sleep at night), you’re not alone. Have you ever thought about real estate as an investment?

When I bring up real estate, many people immediately think about buying a home or condo, or about complex “alternative investments” that are high risk and not very liquid. But real estate is not as intimidating as you might think, and there are many ways to participate. I’ll get to those in a minute. First let’s look at the many benefits of investing in real estate and the multiple ways it can benefit your wealth accumulation and retirement planning.

Real estate is IDEAL

When it comes to real estate, there are five main ways you can win by investing in real estate. In many ways, real estate is an “IDEAL” vehicle for growing and preserving your wealth:

“I” stands for Income – the positive cash flow from the rent you collect minus your expenses on the property.

“D” stands for Depreciation. As your real estate assets depreciate, you can use that deduction as an income offset every year on your taxes. Residential real estate can be depreciated for 27-1/2 years; commercial property for 39 years.

“E” stands for Equity. As you pay down the mortgage or other loan on the property (often with rental income) you continue to build up equity in the property. Essentially tenants are helping you pay off your loan.

“A” stands for Appreciation. Over the long-term, real estate returns 7 percent annually after adjusting inflation, meaning it has outperformed bonds, Treasury bills and even stocks.

“L” stands for Leverage. You only need to put 20% to 25% down to own valuable income producing property.

When it comes to real estate assets, your rates of return are multiple, not just one stream. Let me show you how this works.

Real world example

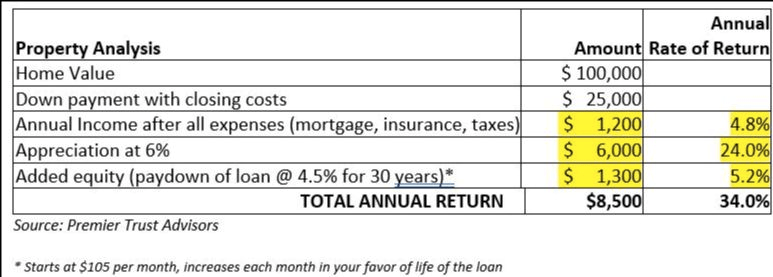

Let’s say you find an attractive property in your price range that you’d like to use as a rental property. After the inspection checks out, the seller agrees to let you have the property for $100,000. You only need to put $20,000 down ($25,000 with closing costs) to acquire the property.

You only need an $80,000 mortgage to carry the property, and at today’s low rates (say 30 year fixed at 4.5%), you might only pay about $405 per month. Further, almost $110 or your monthly mortgage payment goes to principal, so each year you are paying down at least $1,300 in principal. That means you are building up $1,300 per year in equity. Also, the property is generating income when you rent it out. Let’s say it generates an average profit of $100 per month after expenses. That’s $1,200 per year income to you and due to depreciation costs, you’ll likely earn this cash flow tax-free.

Finally, let’s say the property appreciates 6 percent per year on average, which is very realistic as shown above. So, on top of your $6,000 in average appreciation, you receive an additional $1,200 a year in rental income and another $1,300 a year minimum in equity built up as you pay down the loan. That’s $8,500 per year on a $25,000 initial investment (i.e. 34%)!

Conclusion

This is just an example showing how real estate over the long-term can outperform all of the other asset classes you are likely to own, including stocks. By the way, you don’t have to be the actual owner of a property to participate handsomely in real estate. We’ll discuss more in my next post.