Key Takeaways

Even well-educated, financial savvy professionals can find themselves short on liquid cash when life comes their way with the unexpected.

Did you know your savings and retirement accounts contain plenty of hidden risks?

There are ways to build substantial wealth without losing control or exposing yourself to excessive risk. Read on for more.

There is still significant uncertainty over COVID, the direction of the economy/inflation and the potential correction in asset prices. Taking personal responsibility for your money is the best way I know to build and preserve your wealth during uncertain times.

Since October is National Financial Planning Month, it’s a good time to reevaluate whether you’re still on track with your financial goals and objectives. It’s not always fun but doing so not only boost your odds of having a secure retirement and financial future, but it puts you way ahead of most Americans.

A Gallup survey found that only 3 in 10 Americans have a long-term financial plan. And Employee Benefit Research Institute found more than two thirds of Americans (70%) think the main way to ensure a comfortable retirement is to keep working.

As I’ve always said: “Hope is not a strategy.”

Savings is the foundation of a good financial plan at any age in any economic climate. But, with interest rates so low (i.e., penalizing savers) savings has become a lost art.

It shouldn’t be.

To clarify, saving is money that you’re accumulating that only goes in one direction…up. There is essentially little risk of your principal being lost. And, you easily have access to the funds whenever you need them. Most think plunking money in a 401(k) retirement account is a form of saving, but it’s actually a risk asset since the value of the account can fluctuate with the financial markets and you can’t access that money without penalty until age 59 ½.

Again, investing is using money that you’re trying to grow—but of course, that comes with risk of loss. You need low-risk liquid savings to stock your emergency cash fund (6 to 12 months of basic living expenses). In addition to your emergency cash, you need additional liquid savings to take advantage of business or investment opportunities that come your way unexpectedly. For many people, the only think worse than losing money, is not having enough liquid cash to take advantage of a great opportunity.

You also need liquid savings to finance the down payment on a new home or to pay for college. If you think you’ll be needing to tap your money sooner, do you want to put it at risk and possibly not have enough? Also, if you don’t have savings available and something happens, you may have to liquidate your investments with potential penalties or tax consequences. You might also need to utilize expensive debt such as a credit card which can reach very high rates.

All too often, even well-educated, financial savvy professionals can find themselves short on liquid cash when life comes their way with the unexpected.

It doesn’t have to be this way.

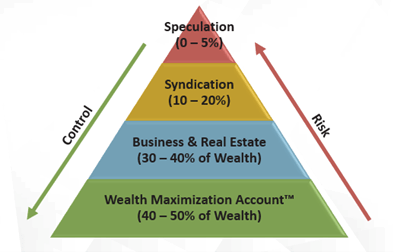

Introduce Hierarchy of Wealth to help guide your portfolio.

Did you know there is a way to build wealth without exposing yourself to excessive risk and to gain more control over your money than qualified retirement plans and stock market investments?

It’s called The Hierarchy of Wealth developed by Paradigm Life.

Just like Maslow’s Hierarchy of Needs for personal survival and fulfillment, there is a natural hierarchy for meeting your financial needs: fulfill the most essential first before pursuing any other comfort goals or aspirational financial goals. The first step in the Hierarchy of Wealth is to secure your financial foundation through a Wealth Maximization Account™. Your WMA is a properly structured whole life insurance tool that provides access to cash value, tax advantages, compound interest, and other benefits that help grow and protect your wealth.

In essence, the Hierarchy of Wealth is a way to balance control and risk in your financial life. Conventional wisdom is that we need to take on greater risk (i.e., stocks) in order to achieve higher returns on your money. However, if you have better control of your assets, you can actually reduce your level of risk while still receiving sizable returns. So many people start thinking about investments before they build a solid financial first. Unfortunately, a house with a weak foundation can come crumbling down when a storm hits.

Don’t make that mistake.

The Hierarchy of Wealth is a better way to preserve your assets and achieve your goals.

Tier 1 (WMA): At the base of your pyramid (see above) is where you protect yourself and your family from key risks such as death, disability, and lawsuits. It’s also where you store well your cash reserves such as bank accounts, money market, CDs and cash value life insurance. Your WMA guarantees those reserves against loss and make the money accessible whenever you need it. Level 1 is the safe and liquid part of your financial life and not the area where you’re seeking high returns. A sizable portion of your wealth—say, 40% to 50% — should start here before you begin putting your money at risk.

Tier 2 (Business & Real Estate). Once you establish Tier 1, you work your way up the hierarchy into investments that you can control and influence. These include investments in your professional education, your personal developments, and networks. Your No.1 asset is you and your ability to provide value to the most important people in your life.

Tier 2 can also include assets that grow and create income, such as your own businesses or direct ownership of rental real estate. Both businesses and rental real estate give you greater control than the stock and bond markets do, plus they throw off growth, income, and tax benefits. Many clients keep 30% to 40% of their assets in Tier 2 and you can leverage money from Tier 2 to finance them.

Tier 3 (Syndication). Here is where you can take on more risk, such as start-up businesses, investments and assets that have collateral, but are controlled by others such as private lending and real estate syndications (e.g., apartment buildings, self-storage, mobile home parks) that are backed by assets. Because there is a degree or risk here, don’t allocate more than 10% to 20% of your assets to Tier 3.

Tier 4 (Speculation). Here is where you can on more risk by investing in assets that you neither control nor influence—assets that are not backed by collateral. This is where you allocate a smaller portion of your assets (i.e., 5%) to invest in stocks, bonds, mutual funds and even cryptocurrency–since you have the least control and the highest degree of risk.

Conclusion

If you or someone close to you has concerns about their retirement plan or portfolio risk , please don’t hesitate to contact me to schedule a Discovery Session.

Also, come join our private Facebook group to connect with others looking to gain control over their finances.

Prosperity is within your control.